© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 1 of 6

Mortgage Insurance (MI)

Plan Comparison, Questions and Answers, and Examples

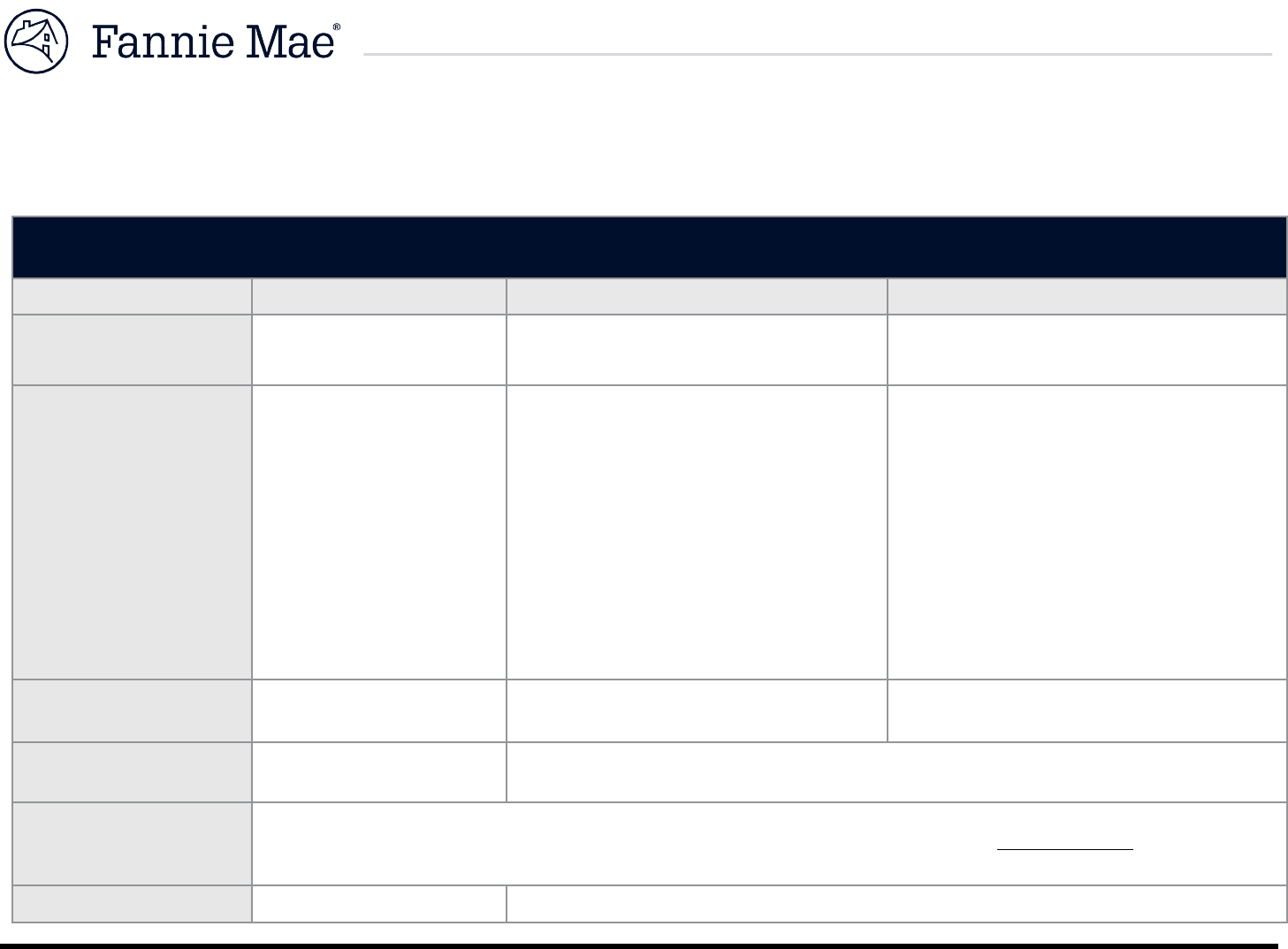

MI Plan Comparison

Monthly Premium

Single Premium

Split Premium

MI Payment Description

No upfront MI premium,

premium paid monthly

One-time upfront MI premium with no ongoing

MI payments

Both an upfront MI premium and monthly MI

payments; features multiple upfront premium

options with corresponding ongoing premiums

Payment Options

Borrower pays monthly

The upfront premium can be paid at

closing by the borrower, an

interested third party (subject to

contribution limits), or financed into

the loan amount.

OR

Lender buys the MI and increases

borrower’s note rate or discount

points to indirectly cover the cost of

the MI premium.

The upfront premium can be paid at

closing by the borrower or an

interested third party (subject to

contribution limits). It can also be

financed into the loan amount.

The ongoing premium is typically paid

by the borrower.

If lender-paid, the cost of the upfront

and ongoing MI premiums will be

added to the borrower’s note rate or

discount points.

At Closing

Monthly premium required

for escrow

Entire MI premium amount is due

One-time upfront MI premium paid at closing

plus monthly premium required for escrow

Net (base) LTV

1

for

Loans with Financed MI

N/A Used to determine required MI coverage percentage

Max LTV or Gross LTV

2

for Loans with

Financed MI

97% (for LTVs >95% up to 97%, the transaction must qualify for one of the 97% LTV Options)

MI Coverage

Based on LTV Based on LTV or Net LTV when all or a portion of the MI premium is financed

© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 2 of 6

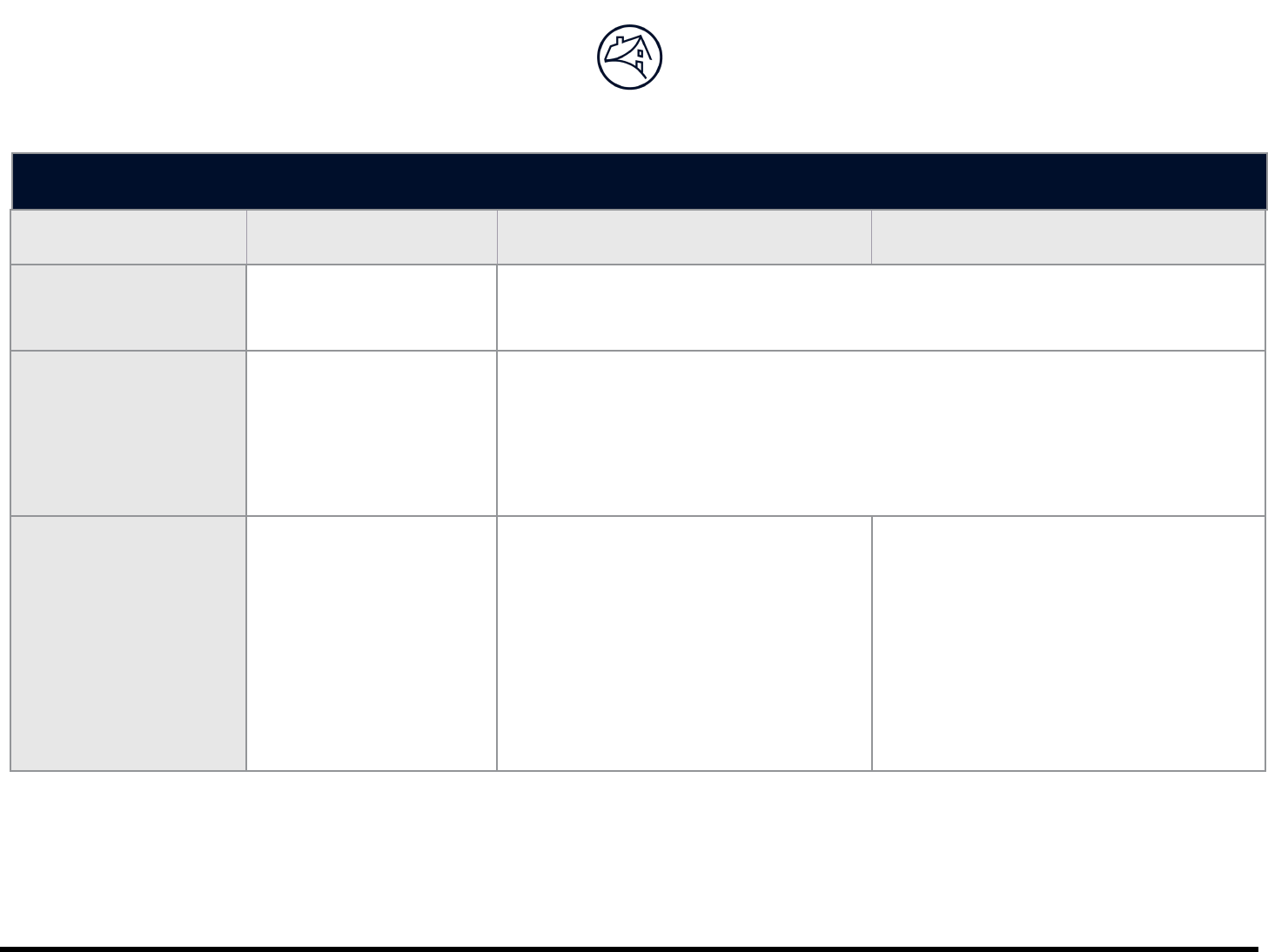

MI Plan Comparison

Monthly Premium

Single Premium

Split Premium

Fannie Mae Eligibility

Requirements and

LLPAs

Based on LTV

Based on LTV or Gross LTV when all or a portion of the MI premium is financed

For lender-

purchased MI,

restrictions exist for

convertible ARMS.

(See the Selling

Guide.)

Mortgage loans with financed mortgage insurance must be purchase, construction, or

limited cash-out refinances (LCOR) for one-unit principal residence or second home

Other Eligibility

Restrictions

Borrower Benefit

No add-on to note

rate or loan amount

No upfront MI

premium cost

Highest potential tax deduction

benefit since cost is either financed

in the loan amount or funded

through a higher note rate

3

Generally with financed single

premium, PITI will be lower than if

the MI premium is paid monthly

Generally with financing the upfront

portion of a split premium, PITI is

lower than if the entire MI premium

is

paid monthly

© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 3 of 6

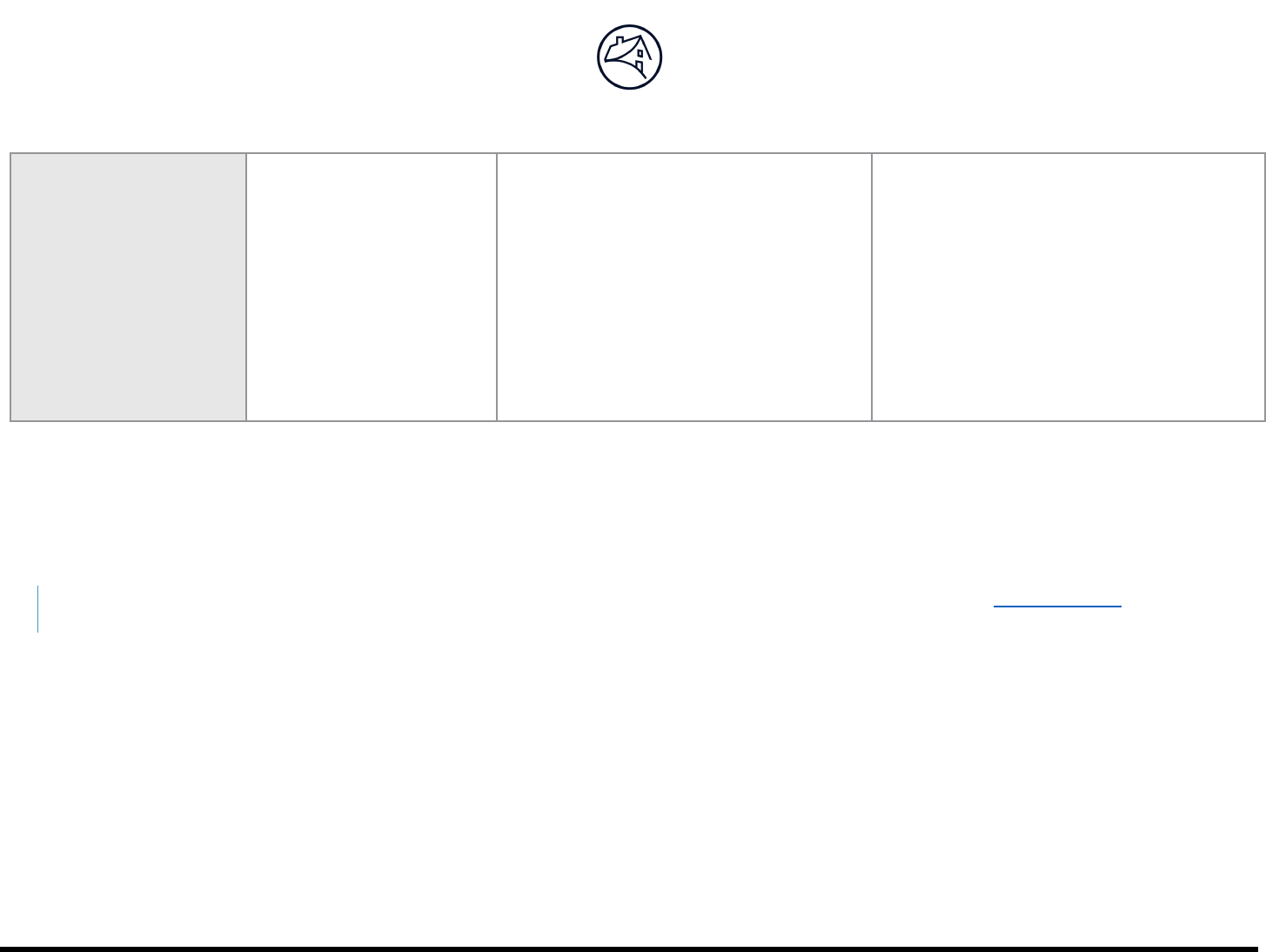

Other

Considerations

No tax benefit for

MI premiums paid

after 2016 unless

Congress extends

the tax benefit

3

Generally produces

the highest monthly

mortgage payment

for the borrower

Increased UPB and more interest

over the life of the loan if financed

into the loan amount

Higher initial cost to borrower if

borrower-paid

If not financed, results in higher

closing costs for the borrower

All or part of upfront MI cost may be

included in Qualified Mortgage (QM) pointes

and fees limit

4

Increased loan amount or note rate,

based on financing option for the

upfront portion

If not financed, results in higher

closing costs for the borrower

All or part of upfront MI cost may be

included in QM points and fees limit

4

Notes

1 Net LTV is calculated without the MI premium.

2 Gross LTV is calculated with the partial or lump sum MI premium included in the loan amount.

3 Fannie Mae does not provide tax advice. Borrowers should confirm the tax effects with their tax advisor.

4 Need to consider the implications of upfront MI for compliance with Fannie Mae’s Selling Guide provisions on points and fees, as well as those required by the Consumer Financial

Protection Bureau.

NOTE: Information contained in this summary is for informational purposes only. Refer to Fannie Mae Selling Guide section B7-1-01, Provision of

Mortgage Insurance and the insurers’ guidelines, for complete mortgage insurance requirements.

© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 4 of 6

Questions and Answers

Q1. What is the difference between a “financed MI transaction” and a “prepaid MI transaction”?

These are the two options Fannie Mae provides to lenders for limited cash-out refinance transactions in which MI is included in the loan amount.

The key difference between the two transaction types is how the MI cost is treated and how the MI coverage requirement is calculated.

Financed MI transaction

The lender must identify the upfront financed MI amount separately and follow Fannie Mae’s requirements for entering in Desktop

Underwriter® (DU®) and coding for loan deliveries.

The MI coverage requirement is based on the net LTV (i.e., the LTV without inclusion of the financed MI amount).

This approach typically offers the best solution when

• lenders are looking for a simplified operational approach to address limited operational capabilities for financed MI, and/or

• the financed MI amount is substantial enough to make a difference in the required MI coverage percentage when comparing the

net LTV and gross LTV (e.g., financing a split- or single-premium MI plan – see examples on page 6).

Prepaid MI transaction

Treat upfront MI amount as a prepaid item at closing. Lenders need not separately identify the upfront financed MI amount; it is simply

included with other allowable prepaid closing costs.

There are no special DU data entries or delivery coding requirements – the loans are treated as any other limited cash-out refinance.

This approach typically offers the best solution

• with smaller MI amounts (e.g., escrows related to monthly MI rate plans, or some portion of upfront annual or split premiums) that

would have little or no impact to the required MI coverage percentage.

A potential drawback with this method is that the net LTV cannot be computed, so the required MI coverage may be higher than it would

be under a financed MI transaction.

NOTE: The total LTV for both transaction options must meet the LTV limits in Fannie Mae’s Eligibility Matrix for loans with the corresponding loan

characteristics.

© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 5 of 6

Q2. What are the eligibility requirements for loans with financed MI?

Loans eligible for financed MI are limited to one-unit purchase, construction, or limited cash-out refinance for principal residences or second

homes.

Q3. What are the eligibility requirements for loans with prepaid MI?

Prepaid MI is limited to refinance loans only and may include closing costs, prepaid items, and points in the loan amount.

Q4. Why does Fannie Mae require more MI coverage under the prepaid MI option than under the financed MI option?

With financed MI, the upfront MI amount being financed is identified separately and the lender obtains an “endorsement” to the MI policy, which

says that, in the event of a claim, the policy fully covers the portion of the loan that is the unamortized portion of the loan amount relating to the

financed MI premium. As such, Fannie Mae’s exposure is no more than it would be if the borrower did not finance the MI – which is why Fannie

Mae permits the coverage percentage to be computed using the net LTV. However, with prepaid MI, because the upfront MI amount being

financed is not broken out separately and is lumped in with other closing costs, the MI company cannot provide its typical financed MI policy

endorsement; therefore, Fannie Mae’s exposure is based on the total LTV, including the closing costs with the upfront MI amount embedded. So,

it is important to recognize that borrowers can get the best execution in terms of required MI coverage with lenders who offer and are operationally

capable of using the financed MI option.

Q5. What special feature code should be used in delivering a mortgage loan with financed MI?

Special Feature Code 281 is used to identify mortgages that have a borrower-paid mortgage insurance premium that is financed in whole or in part

into the loan amount. The gross LTV ratio is determined after the financed premium is added. The mortgage insurance premium is determined

before the premium is added to the loan amount.

Q6. Does the “ability to repay” rule published by the Consumer Financial Protection Bureau (CFPB) have any impact on MI premiums?

Certain MI premiums must be included in the points and fees tests that we apply. Lenders must comply with our policy requirements as well as

CFPB standards for determining the circumstances for inclusion or exclusion.

© 2017 Fannie Mae. Trademarks of Fannie Mae. March 2017 6 of 6

Limited Cash-Out Refinance Examples

Example 1

Single Premium –

Financed MI

Example 2

Single Premium –

Prepaid MI

Example 3

Monthly Premium Escrow –

Prepaid MI

Home Value

$254,000

Current Loan Balance

$225,000

Closing Costs/Prepaid Items/

Points (excluding upfront MI)

$3,500

Net Loan Amount

$228,500 [$225,000 + $3,500]

Standard MI Coverage Required

(sample rates based on credit

score 740, FRM 30-yr, owner-

occupied)

Net LTV 90%, MI coverage of 25%

Rate: 1.37%

LTV of 95%, MI coverage of 30%

Rate: 2.15%

LTV of 90%, MI coverage of 25%

Rate: 0.41% annually, 2 months

escrow

Upfront MI Cost

(all plans except single-premi-

ums require ongoing monthly

MI payments not shown here)

$3,130

Computation: 1.37%

x $228,500

$4,961

Computation:

[2.15% x $228,500] ÷ (100% - 2.15%)

$156

Computation:

[0.41% x $228,500] ÷ 12 x 2mos

Financed Loan Amount

$231,630

(=$228,500 + $3,130)

$233,461

(=$228,500 + $4,961)

$228,500

Final LTV with Closing Costs

and MI Premiums Financed in

Loan Amount

91.2%

(=$231,630

÷ $254,000)

91.9%

(=$233,461 ÷ $254,000)

90.0%

(=$228,500 ÷ $254,000)

LTV Used for MI Coverage

90%

(=($228,500)

÷ $254,000))

91.9%

(=$233,461 ÷ $254,000)

90.0%

(=$228,500 ÷ $254,000)

Notes

Example 1: This loan uses a single-premium MI plan that will be financed in the loan amount. The loan is submitted in DU as a financed MI transaction, allowing the MI cost to be excluded

from the LTV calculation, resulting in a premium based on 90% LTV (see above). The loan amount and financed MI amount are entered in DU separately.

Example 2: This loan also uses a single-premium MI plan that is included in the total financing, but the MI cost is submitted in DU as a prepaid item. This results in an LTV inclusive of MI cost

that exceeds 90%, so the required standard MI coverage is 30% (for the 90.01–95% LTV category).

Example 3: This loan uses a monthly premium MI plan requiring two months to be escrowed at closing that will be included in the closing costs that are added to the loan amount. Note that MI

companies also offer monthly premium plans that do not require upfront escrows, in which case this example would not apply.

Examples contained in this document are for illustrative purposes only.

Actual results will vary depending on the individual characteristic of each loan and the required MI premiums.